Second Quarter, 2023

Click here for a printable version of the Investment Update.

July 7, 2023 – This is a quarterly update of economic conditions and investment strategy.

A Positive First Half Despite Persistent Unease

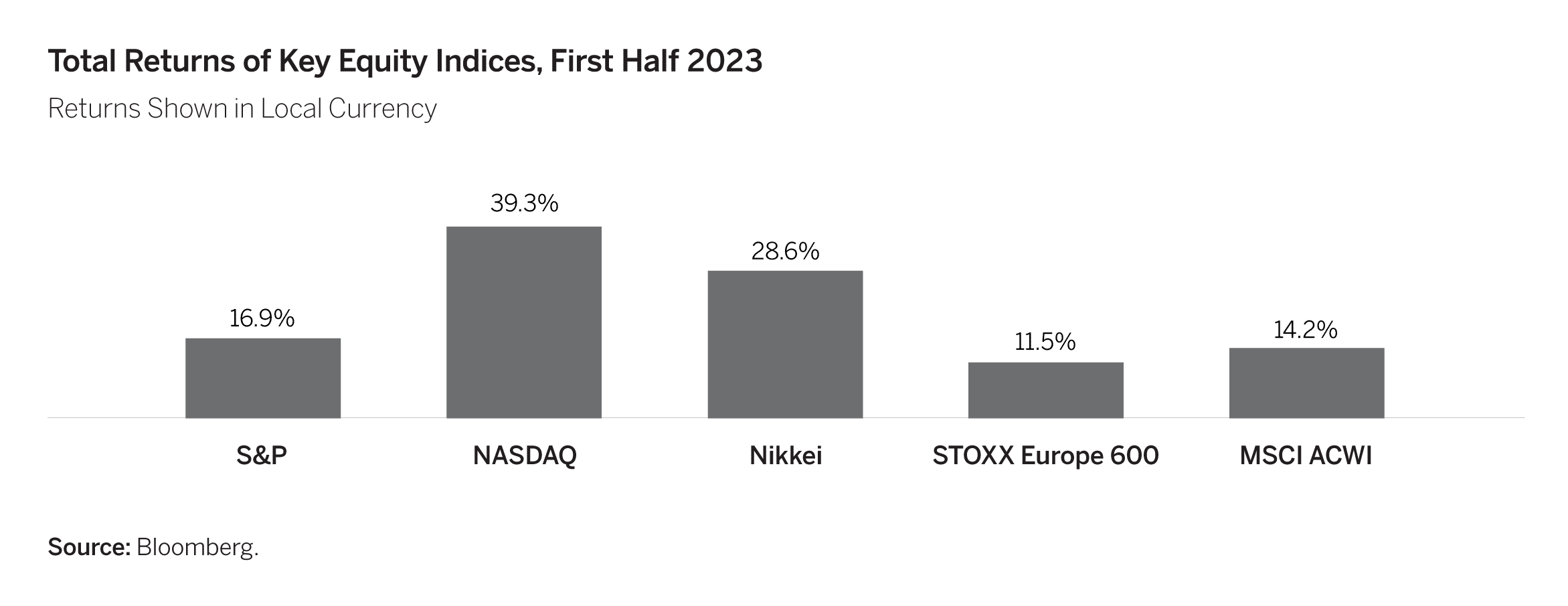

U.S. and global equity markets continued to climb in the second quarter of 2023. The S&P 500 generated a total return of 8.7%, bringing the Index’s year-to-date return to an impressive 16.9%. The NASDAQ did even better, returning 39.3% in the first half of 2023 after declining over 32.5% in 2022. Japanese and European equities were also very strong. Japan’s Nikkei Index returned 28.6% in the first half, and the STOXX Europe 600 returned 11.5%. The MSCI All-Country Index (MSCI ACWI), which includes both developed and developing markets, returned 14.2% for the first half of 2023.

Bond markets were generally unexciting in the first half of 2023, a welcome change after the declines of last year. In the U.S., bonds generated low single-digit returns, with long-term yields trading in a relatively narrow range in the second quarter. At the end of the quarter, U.S. short-term Treasury Bond yields hovered around 5%, and long-term yields were approaching 4%.

Generally speaking, investors entered 2023 with low expectations. Central bank tightening around the world in 2022 led to concerns of recession and declining corporate earnings. However, macroeconomic data have proven stronger than expected and inflation has declined. In the U.S., real income growth turned positive for the first time in two years.

If inflation continues to fall as we expect and U.S. economic growth continues to exceed investor expectations, the U.S. equity market rally will likely continue for at least a few more months. However, we think it is far too soon to conclude that a recession has been averted or that this is the beginning of another bull market in U.S. equities.

Traditional leading economic indicators still indicate a slowdown is coming. The Federal Reserve is still restricting the money supply, banks are tightening lending standards, and business demand for credit is contracting sharply.

In addition to maintaining our focus on macroeconomic and financial market developments, over the past six months we have made important strides in our Thematic Equity research. We devote the remainder of this Update to sharing how this work has led us to important advancements in several themes and how they are represented in clients’ portfolios.

During the first half of 2023, we introduced one new theme, retired another, substantially revised a third, and adjusted the weights of others in response to our Thematic research findings, financial market movements and macroeconomic shifts. Our new positioning reflects our latest views of the near- and long-term risk and reward prospects for each theme.

Retired Theme: Long-Term Covid Beneficiaries

We initiated this theme in the third quarter of 2020 to capture opportunities created by abrupt changes in consumer behavior during the Covid pandemic. While it was clear some of these changes were temporary, we expected others to endure, particularly those that increase productivity or enhance the consumer experience.

Many of these changes are now much better understood – and valued – by investors, so some of the investment opportunities have become less compelling. Those companies we identified as part of this theme that have advantages we see as more enduring and investable are now incorporated in the Converging Consumer theme.

New Theme: Opportunities Abound Abroad

Non-U.S. equities have vastly underperformed U.S. equities over the past 15 years. The MSCI All-Country World Index, excluding the U.S., has delivered a cumulative return of just 54% since May 1, 2008, while the S&P 500 has delivered a whopping 335% cumulative return. Driving this wide gap in market returns were geopolitical and macroeconomic factors abroad and a confluence of circumstances in the U.S. that are unlikely to persist.

In several developed markets outside the U.S., structural reforms in fiscal, energy and industrial policy and in capital markets rules are beginning to take hold. We believe these changes will lead to better equity performance in both Europe and Japan for years to come.

The Case for Europe At the end of 2007, the European stock market, represented by the STOXX Europe 600, was almost as large as the U.S market, represented by the S&P 500. At the end of 2022, the S&P 500 was roughly 2.6 times larger than STOXX Europe 600.

Today, many of the issues that have plagued Europe over those 15 years are abating, while some U.S. advantages are fading. Specifically:

-

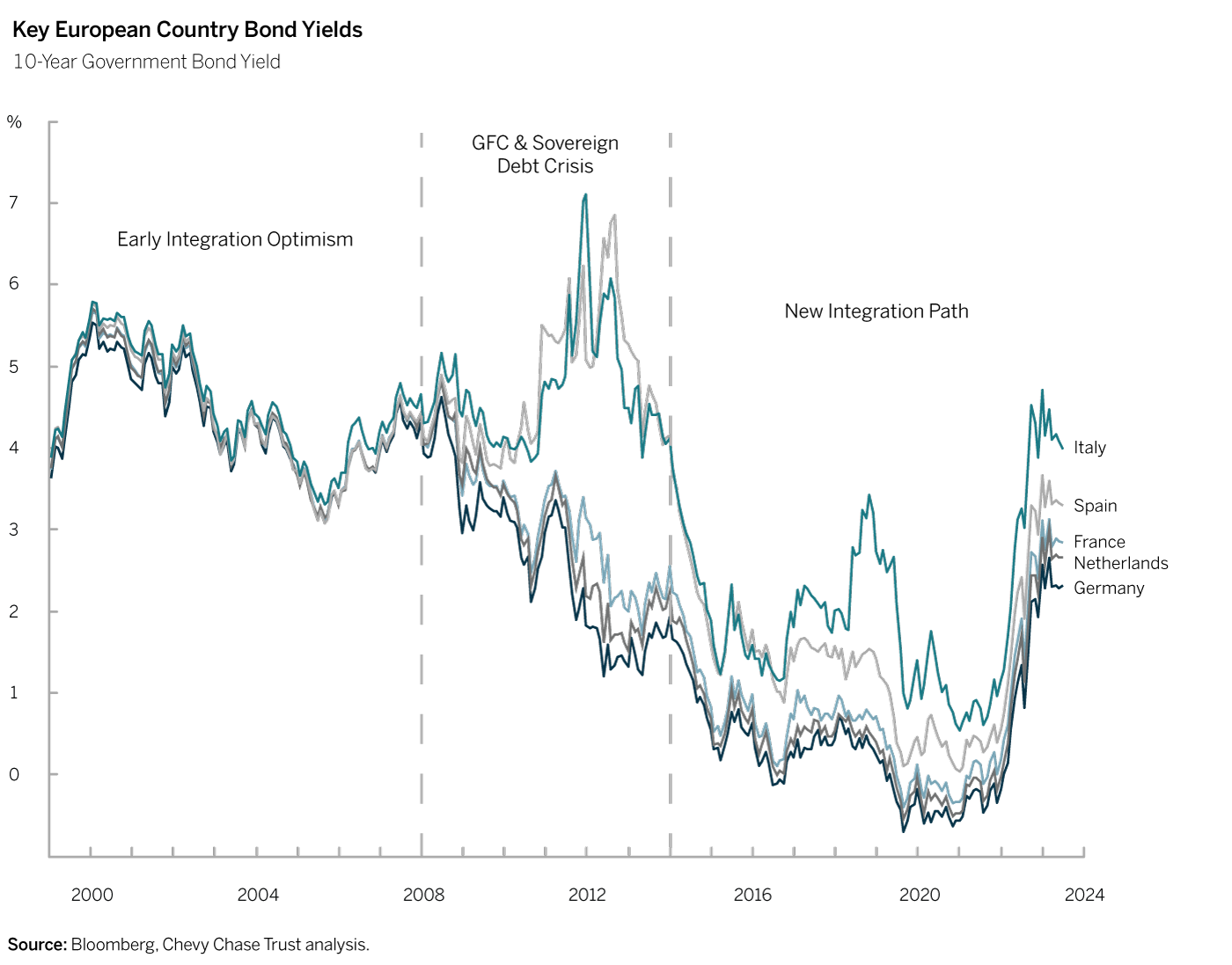

- Growing Support for European Integration A decade ago it was far from clear that the European Union (E.U.) would persist. The E.U. was established in 1993, with the Euro coming into use several years later. During the 2011-12 European Sovereign Debt Crisis, many investors believed the Union might not hold. Credit spreads widened between different countries as fears grew that some would be forced to abandon the Euro. At the time, only about half of the public supported the E.U. Today, public support for the E.U. is at an all-time high, with 80% of Europeans fully supporting economic unification. Furthermore, the E.U. itself can now issue debt, a significant step forward in the integration process.

- Growing Support for European Integration A decade ago it was far from clear that the European Union (E.U.) would persist. The E.U. was established in 1993, with the Euro coming into use several years later. During the 2011-12 European Sovereign Debt Crisis, many investors believed the Union might not hold. Credit spreads widened between different countries as fears grew that some would be forced to abandon the Euro. At the time, only about half of the public supported the E.U. Today, public support for the E.U. is at an all-time high, with 80% of Europeans fully supporting economic unification. Furthermore, the E.U. itself can now issue debt, a significant step forward in the integration process.

-

- Movement Away from Austerity After the 2008-09 Global Financial Crisis (GFC), the E.U. adopted monetary and fiscal policies to stimulate an economic recovery, despite the aversion to debt-fueled spending and inflation that had long dominated many European institutions. Soon after the worst of the crisis was past, the E.U. reverted to type, raising interest rates and requiring member countries to rein in fiscal spending and repay bailout loans extended during the GFC. These actions contributed to the double-dip recession on the Continent, while the U.S. economy continued to strengthen. It appears European policy makers have learned from that mistake. In our view, the E.U. has recently adopted more stimulative policies, and the European Central Bank (ECB) has been raising interest rates at a slower pace than the U.S. Federal Reserve, despite generally higher levels of inflation.

-

- Better Energy Policies The importance of energy to both manufacturing and services cannot be overstated. For most of the past decade, average energy prices in the E.U. were double the U.S. average, due to higher taxes and strict renewable energy policies. Energy shortages brought on by the Russian-Ukraine war led some European countries to soften their opposition to fossil fuels and will likely lead to more rational strategies and lower energy costs going forward.

-

- A Fuller Embrace of Trade Free trade is good for economic growth. Countries that embrace international trade tend to grow faster, innovate more quickly, enjoy larger gains in productivity and provide higher income and more opportunities to their people. Tariffs raise the cost of goods for consumers and tend to lower corporate margins. After declining for decades, U.S. tariffs started to climb in 2017. While the U.S. appears to be adopting more protectionist policies, Europe is entering into more trade agreements than the U.S. and has avoided taking an overly belligerent stance toward China.

-

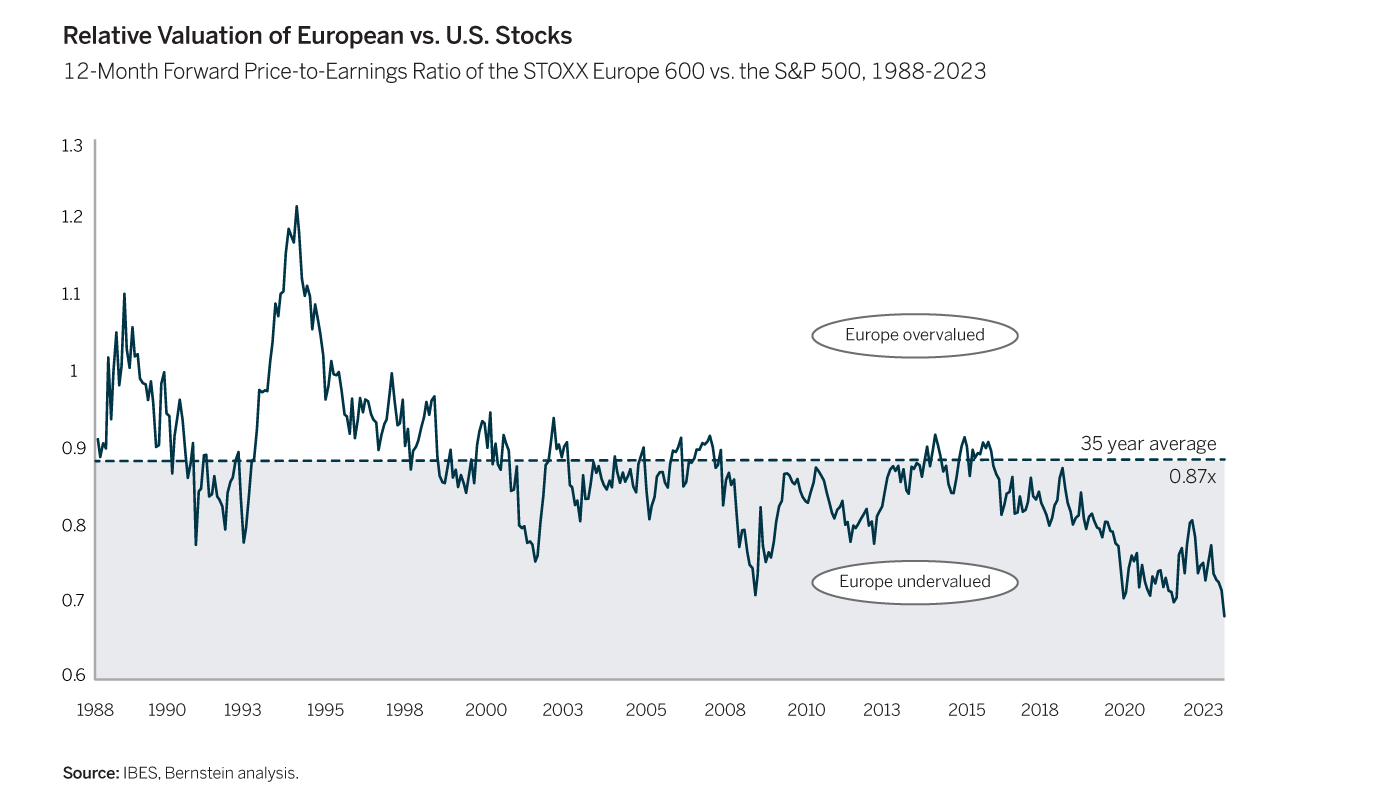

- More Compelling Valuations With a 12-month forward price-to-earnings ratio of 12.2 compared with 19.4 in the U.S., European companies are available at compelling valuations. Their average discount to U.S. stocks is now wider than it has been for many years.

- More Compelling Valuations With a 12-month forward price-to-earnings ratio of 12.2 compared with 19.4 in the U.S., European companies are available at compelling valuations. Their average discount to U.S. stocks is now wider than it has been for many years.

The Case for Japan The investment case for Japan is quite different – but also compelling. The Nikkei Index is finally approaching the peak it first reached 34 years ago, just before its spectacular bubble burst. Meanwhile, the Tokyo Stock Exchange (TSE) is adopting policies that should make equities more attractive to investors, propelling further gains.

The size of the bubble in Japanese equities was truly historic. In 1989, half the world’s stock market capitalization traded on the TSE, compared to only 25% on the New York Stock Exchange. In just five years between late 1984 and late 1989, the Nikkei soared from 10,700 to 38,800. Its deflation was equally historic and unusually long-lived. By late 1990, the Nikkei declined 35%, to 24,000. The index continued to trend lower for much of the next 13 years. In 2003, it briefly dipped below 8,000, almost 80% below its peak 14 years earlier. After 2003, the Nikkei once again doubled, before falling back to its 2003 lows during the GFC.

It is hard to overstate the psychological impact on investors and management teams of the bursting of such a huge bubble. The impact is still evident in several ways:

-

- Low equity allocations After years of underperformance, local ownership of Japanese equities remains exceptionally low. For example, Japanese pension funds currently allocate only 11% of their portfolios to Japanese equities, and Japanese insurance companies, only 6%. U.S. pension funds and insurance companies, by contrast, allocate 30% and 11% to U.S. equities, respectively.

-

- Extremely low valuations Trading at an average of 1.3x book value, Japanese equities are much cheaper than their U.S. counterparts, which trade on average above 3.5x book.

-

- Corporate cash hoards More than half of Japanese listed companies have positive net cash (after adjusting for debt), compared to less than 20% of their U.S. and European peers.

To make Japanese equities more attractive to investors, the TSE recently issued new mandates for companies that trade below book value. The management and boards of directors of each of these companies must assess their cost of capital and capital efficiency and disclose a plan to improve capital efficiency, share price and market capitalization.

Japanese non-financials, in particular, have plenty of scope to hand more of their ¥350 trillion ($2.5 trillion) cash pile to investors, who can reinvest it elsewhere – or in Japanese stocks likely to rise in value when not weighed down by excessive cash. We see opportunities in Japanese banks and trading companies, as well as global suppliers of automation equipment and other productivity-enhancing industrial technology.

Mega Tech May Start to Weigh on the U.S. Stock Market Many find it hard to imagine European and Japanese markets leading the U.S. market after more than a decade of great performance by the U.S. and subpar results from Europe and Japan. But U.S. stock market leadership over the past two decades was powered by a small group of large-capitalization technology or tech-related stocks, each of them essentially a monopoly generating huge and rapidly growing cash flows. Ultra-low interest rates increased the present value of their very high expected growth, and these stocks ballooned in value.

The huge winners of the past decade – Facebook, Apple, Amazon, Microsoft, Netflix, Google, and Tesla – are highly unlikely to be the big winners of the next decade. They have become so big that they can no longer grow as quickly as they once did, and interest rates are higher, reducing the present value of their expected growth. Apple’s market capitalization alone is already larger than the entire market capitalization of the FTSE index of U.K. stocks, and twice the market cap of the entire German stock market.

Thematic Evolution: From Increasing Wealth Concentration to Converging Consumer

Our Increasing Wealth Concentration theme initially focused on opportunities created by the increasing concentration of U.S. wealth in urban areas. We saw that consumers who lived in dense urban areas had different consumption patterns from consumers spread out in the suburbs and rural areas. We also saw that the companies catering to urban consumers benefited from this greater population density. In this respect, the consumption patterns of wealthy U.S. consumers were growing increasingly like the pattern for their overseas counterparts, who mainly lived in big cities, not suburbs.

While the pandemic changed the pace of urbanization we had expected, it hastened other changes in middle- and upper-class consumer behavior across geographies.

Prior to Covid, consumers in many Asian countries shopped more online than their U.S. and European counterparts. Then, pandemic-related store closures, work-at-home mandates and fiscal stimulus drove consumers online globally. Many consumer products companies learned to use the Internet to engage more directly with end users, moving away from a reliance on traditional physical retailers.

Companies with global brands, direct consumer relationships and the ability to manage complex supply chains now have an advantage. Suppliers to these retailers and businesses that facilitate fulfillment of online purchases should also benefit from the shift to direct sales.

Reweighted Themes

We have adjusted the relative weightings of themes in our model portfolios, based on our outlook for financial markets and the macroeconomic environment, as well as advances in our Thematic research. Of note, we trimmed our End of Disinflationary Tailwinds theme because we expect inflation to moderate in the short-term. We reallocated the proceeds from these sales and from exiting our Long-Term Covid Beneficiaries theme into our new Opportunities Abound Abroad theme and our Converging Consumer, Next-Generation Automation and Dawn of Heterogeneous Computing themes.

End of Disinflationary Tailwinds In the first half of 2023, we trimmed this theme, which we had initiated in late 2020 when most investors thought the disinflation of the prior decade was firmly entrenched. We thought vast pandemic-related monetary and fiscal stimulus, coupled with low levels of consumer leverage and commodity supply shortages, would push up inflation in the near term. Perhaps more importantly, we predicted – and continue to believe – that after this short-term spike, inflation would moderate but remain notably higher than it had been for the prior decade.

Our conviction in our long-term inflation outlook remains strong. However, we expect an economic slowdown in the U.S. and other major markets to lead to lower inflation over the next several months, prolonging recent weakness in many of this theme’s holdings.

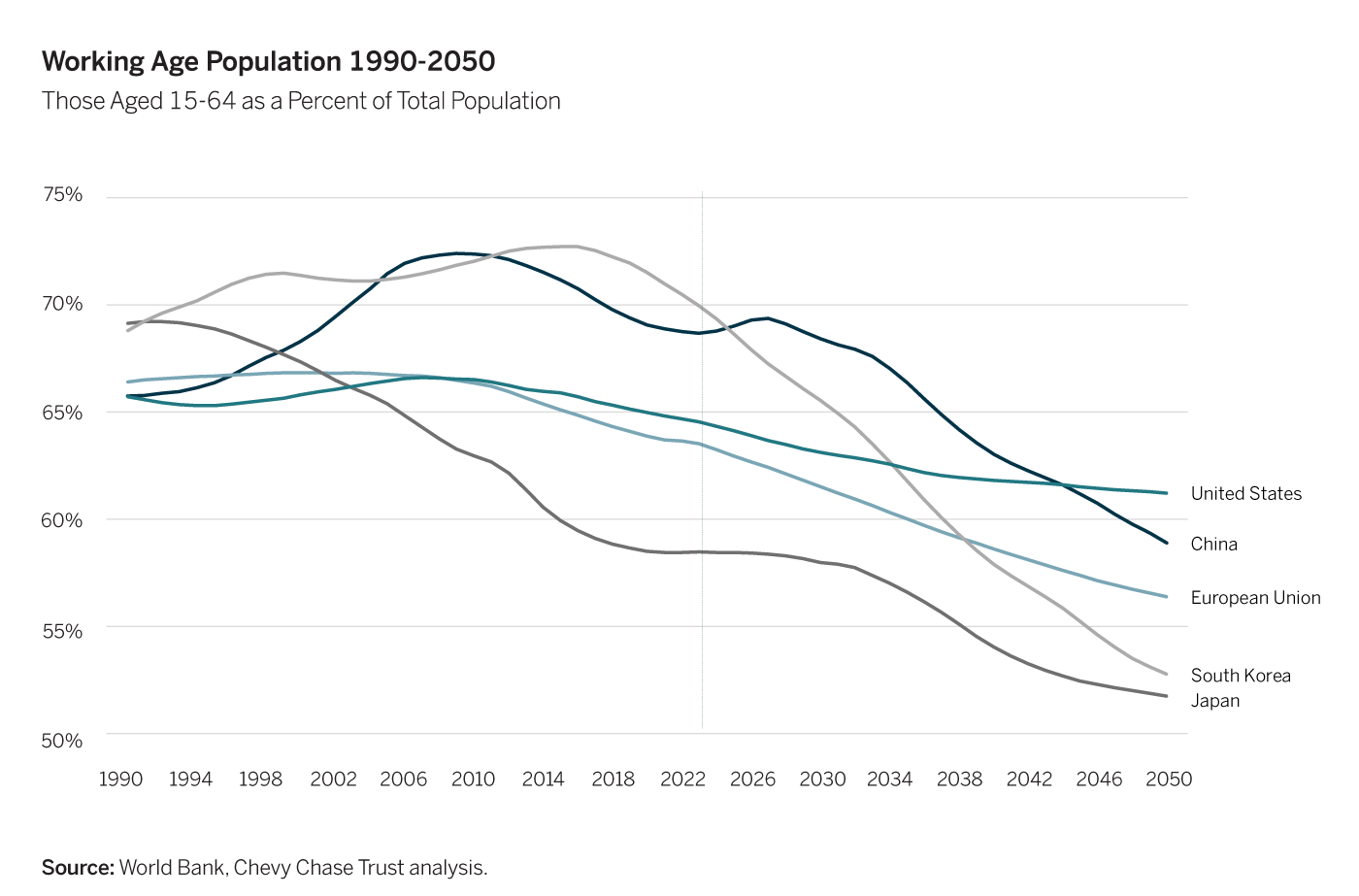

Next-Generation Automation This theme seeks to profit from advanced technologies and new business models that improve productivity and efficiency. Demand for these technologies is now growing, largely because demographic changes are tightening the labor supply globally. In all major economies, the share of the population older than 65 is rapidly growing, and the growth in the working-age population is slowing, if not declining. As a result, wages have started to rise. We expect capital investments in labor-saving technologies to cut costs, improve corporate profitability and increase overall economic productivity, the ultimate source of prosperity.

Advanced automation technology is a broad category that includes autonomous robots, machine vision, lasers, and tracking tools, such as ultra-high frequency radio frequency identification (UHF RFID). Until recently, only very large firms producing a large volume of big-ticket goods, such as cars, could afford the high upfront cost of purchasing robots and integrating them into their production process. Now, those upfront costs are declining because some advanced technologies require less complex customization. In addition, several firms have begun to offer Robotics as a Service, which allows smaller companies and firms that produce smaller volumes of many products to obtain the benefits of automation without a large upfront cost.

Potential users cut across a wide array of industries. Hospitals buy robotic surgery systems. Retailers use UHF RFID for theft prevention, inventory tracking and self-checkout. Manufacturers and warehouses use robots, advanced conveyance systems, UHF RFID, and machine vision. Other industries as diverse as mining and restaurants are also increasing productivity through automation. We are seeking to invest in both companies that produce automation technologies and companies that use them effectively.

Heterogeneous Computing For decades after the dawn of the computer age in 1945, the cost and performance of computer chips improved exponentially, as described by Moore’s Law. In recent years, however, additional improvements have been harder to achieve, and firms have had to pay more for them. Companies that help customers develop purpose-built technology solutions and chips tailored to their specific needs will benefit most from this trend.

Heterogeneous computing also enables Artificial Intelligence (AI), which has recently captured the hearts and minds of investors and the news media. AI requires an extraordinary amount of computing power. By one estimate, if Google searches were replaced by AI queries, its annual technology costs would increase by $30 billion and its capital spending would need to rise by $100 billion. Many of our holdings in this theme would benefit from the expected surge in technology expenditure and increased focus on optimizing networks.

Molecular Medicine The Healthcare sector outperformed the S&P 500 in 2022 but has lagged the Index this year. So have many holdings in our Molecular Medicine theme, despite impressive progress over the past year in research, clinical trials and operations at many participants in the molecular medicine revolution.

The continuing decline in the price for gene sequencing has fostered research into an ever-growing number of genetic diseases and related therapies. The number of clinical trials for cell and gene therapies also continues to grow. Just this year the Food & Drug Administration (FDA) approved the first trials of an in vivo (in the body) gene-editing therapy. We also expect the FDA to approve the first CRISPR-based therapy soon, just a decade after the discovery of CRISPR as a method of editing human DNA.

Our investments in Molecular Medicine fall into two buckets: Companies that develop molecular therapies and firms that produce equipment and services needed to understand and treat genetic diseases. Our longer-term confidence in this theme has only increased as we see new clinical trials and cures for diseases that had been untreatable. The human impact of the progress in this theme cannot be overstated.

In Conclusion

Consistent with our four-step investment process, we remain focused on macroeconomic and financial market developments and continue to advance our Thematic research efforts. As facts and conditions change, we will adjust accordingly.

We are grateful for the trust you place in us.